Recently updated on April 21, 2026

Core banking – aka the brain and heart of a bank, its technological foundation – is the central system that connects all the branches of a bank and runs almost all the basic banking activities like account opening, loan management, transaction processing and more.

Being valued at $17 billion in 2024, the market is expected to grow from $19 billion in 2025 to $59 billion by 2032, exhibiting a stunning CAGR of 16.9% during the forecast period.

This back-end system ensures smooth banking operations and is a vital component of success in the modern financial landscape. In this article, let’s explore the intricacies behind the implementation and integration of core banking systems.

Core banking systems are the backbone of modern financial institutions, providing the essential infrastructure for managing customer accounts, processing transactions, and maintaining financial records.

Content:

- Implementation of Core Banking Systems

- Integration of Core Banking with Other Systems

- The Future of Core Banking

- Conclusion

Implementation of Core Banking Systems

While core-banking system implementation is a difficult and costly process, the results are equally as beneficial and pretty much essential for a bank’s longevity. The journey to achieving a fully integrated system, however, is not without its hurdles. Among the key challenges faced during core banking software implementation are:

Challenges of Core Banking Software Implementation

- Complex Architectural Development: Designing a reliable architecture for intricate and diverse banking structures can be a daunting task.

- Translating Bureaucracy into Code: The highly intricate and bureaucratic processes within banking systems are often difficult to translate into functional and executable code.

- Extensive Research Requirements: Gaining a complete understanding of customers and their needs demands comprehensive research and analysis across various banking lines.

- Pressure to Cut Corners: Stakeholders may feel tempted to take shortcuts to reduce costs or accelerate timelines, often leading to incomplete or unsustainable solutions.

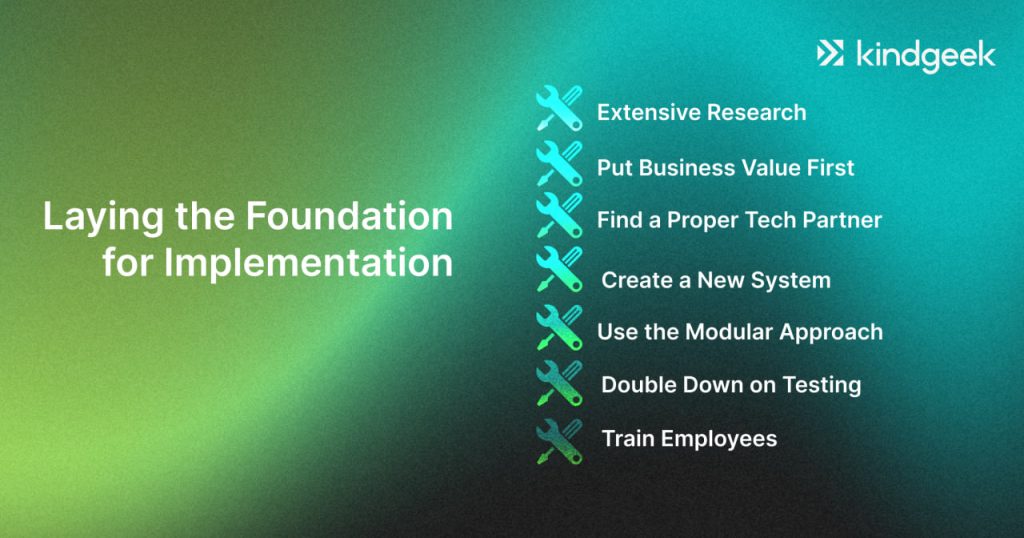

From Challenges to Solutions: Laying the Foundation for Implementation

The challenges aren’t that challenging if you have a nice core banking system implementation strategy at hand. Such a plan, besides involving the base principles of robust and agile software development, should also include.

Extensive Research

Gathering business requirements, analyzing customer base, researching the market to have a complete picture of the future system. When all that you have is an idea, a rough draft, or a vision, we usually recommend conducting the Discovery Phase, so you don’t have to start the development blindly as it may cause a ton of unpredicted costs, time lost, and other obstacles that will hinder the process of creation. Besides, Discovery Phase will provide you with quite accurate core banking system development/implementation costs.

Put Business Value First

The system should be built considering the business value it could deliver. Each important decision should be made relying on technical as well as business aspects of the equation.

Find a Proper Tech Partner

Without mentioning the obvious requirements for expertise and experience, we want to emphasize that the software partner who will develop a core banking system should know how to maintain a balance between committing to requirements expressed by core stakeholders and adhering to the basics of developing reliable and lasting solutions. Such a partner should be a good negotiator with strong product management and business analysis expertise. A company like that would know what it takes to deliver a relevant product to a highly competitive market.

Create a New System

Don’t aim to create a new version of an old core banking system but a brand new system, which caters to the needs of customers to ensure marketability and competitiveness.

Use the Modular Approach

Don’t develop a monolith system from scratch. Develop and deploy a feature, test it in the real environment, and move on to another.

White label banking solution

Consider a white label banking solution. The customizable white-label core allows you to build on top of it and create a unique customer experience. The platform offers a robust infrastructure, ease of integration, and the ability to focus on customer and product experiences.

Double Down on Testing

As we stated previously, QA is the new Black, especially so in FinTech software development. Measure thrice, cut once — you simply cannot over-test a system, therefore, don’t neglect performance, load, integration, usability testing, and all the other flairs of QA meant to uncover hidden issues.

Train Employees

No matter how ideal the core banking system is, it’s important to train employees, so they know how to work with the new software and don’t have to deal with frustrations and a harsh learning curve. A week or two of learning will go a long way in ensuring that the workers will be efficient and not stressed out.

Integration of Core Banking with Other Systems

Integration with a correspondent bank or core banking integration occurs when two banks or financial institutions set up a system to automatically exchange information and perform financial transactions without human involvement.

You might not realize this, but when you transfer money to another company or individual, those funds may pass through several banks before reaching the recipient. If these banks are not properly integrated, each step requires manual data entry and verification, which takes time and increases the likelihood of errors. With integration, all of this is automated, ensuring speed, accuracy, and fewer chances of mistakes.

Key Methods of Integration

API (Application Programming Interface)

Picture two banks wanting to automatically check each other’s customers’ account balances. They can use APIs, which act as a “bridge” for data exchange between them.

File-Based Integration

In some cases, banks use special files to transfer large volumes of data. Imagine a bank wants to send a list of all daily transactions to another bank. Instead of sending each piece of information separately, they can create a special file (like in Excel or CSV format) and transfer it.

Direct Database Access

This method allows two banks to have direct access to each other’s data. For example, if a bank holds information about all account transactions, it can provide access to another bank so that it can verify or update information.

Batch Processing

This method involves banks processing large volumes of transactions through batch data transfers, let’s say, once a day. For instance, a bank may receive transaction files for the day and process them at the end of the day instead of in real-time.

Tips for Choosing a Correspondent Bank

Service Stability and Availability

Before choosing core banking, it’s important to consider the stability and availability of its services. Selecting a bank with well-established customer support can significantly impact the success of the integration. Having prompt and accessible support is crucial.

Cost Considerations

Different correspondent banks may offer varying terms for fees, transaction processing rates, and other financial services. These differences can be significant. Pay close attention to fees for international and domestic transfers, payment processing, and additional charges for using the bank’s services. This can play a critical role in bank selection.

Future Scalability

It’s also important to assess whether the bank can support your future needs. Can it scale alongside your business? Does it support new types of payments and services that you might require as your company grows? This is especially relevant if you’re interested in cards, acquiring, or cryptocurrency in the future.

Security Compliance

Check whether the bank has security certifications and whether it complies with the requirements of financial regulators in your country and international standards.

Integration Technologies

The technologies used for integration, as well as the availability of documentation, can either minimize the time and risks associated with technical issues or, conversely, extend the implementation process and increase costs.

Market Relevance

The market also matters. If you operate in the European market, choosing a U.S. bank may be limited by data processing and transaction requirements. Conversely, for U.S. businesses, selecting European banks may be complicated due to incompatibility in standards.

The Future of Core Banking

As we now gradually move to the age of artificial intelligence, it’s no wonder that the integration of AI and ML into core banking solutions stands vital. Banks can use these advanced technologies to transform their work, making processes like customer service, risk management, and fraud detection smoother and more efficient.

AI and ML are often used in core banking to develop chatbots and virtual assistants that offer efficient and personalized help. These systems can respond to customer questions, handle transactions, and suggest products that match the customer’s financial situation.

Additionally, integrating AI and ML into banking systems can also boost decision-making for financial institutions. These tools analyze customer data and market trends to help banks spot risks, make better decisions, and improve efficiency and profits.

Among other noteworthy trends is the ever-growing emphasis on cloud-based technologies. A growing number of financial institutions are transitioning their core systems to the cloud, which offers scalability, improved security, and cost savings on IT infrastructure.

Another important trend in core banking is the rise of open banking and API-driven architectures. These technologies are transforming finance by allowing banks to connect their core systems with many third-party apps and services, leading to new and innovative financial products that meet customer needs.

On top of that, digital-only banks and neobanks are pushing the demand for agile and easy-to-use core banking solutions. Built on cloud-based platforms, these banks focus on customer experience, data insights, and fast product launches, pressuring traditional banks to modernize.

Consider Kindgeek for fintech software development

Finding a reliable core banking implementation partner could be a challenge though. Such a partner should have not only extensive experience developing highly-protected FinTech applications but also a deep knowledge of the regulatory environment and the modern market state to deliver relevant and competitive solutions. Throwing away the fears of sounding arrogant, we’re confident in our skills and experience developing complex FinTech solutions, and we can handle all the heavy lifting for you efficiently and carefully.

From product discovery phase , core banking implementation, general ledger software development and beyond, we guide through the whole process of developing fintech products. We build software solutions that resolve core business needs with a product-oriented mindset.

Looking for an unique service like custom AI assistant for fintech? We truly have it all to bring your ideas to life!

Conclusion

Developing software for core banking is a rewarding endeavor, with plenty of challenges, a heap of things to consider, and a clear strategic vision to properly implement. Nonetheless, the ‘cost’ of core banking software is reflected in the results it provides. It pushes a bank to a new level of efficiency, helps to retain customers, and provides a great foundation for further innovation. Even though there are core banking software providers, a lot of banks opt for independent development of the system, and rightfully so: the custom system will fit the bank better and will satisfy all its nuanced needs and visions of core stakeholders.

What is core banking in fintech?

Recently updated on September 22, 2025

Core banking refers to the real-time, centralized system that financial institutions use to manage customer accounts, transactions, lending, payments, and other core operations. In fintech, core banking platforms are now cloud-native and API-first, designed for digital-first banking, offering composable microservices and seamless integration with payment rails, lending services, compliance modules, and third-party ecosystems.

How does core banking benefit digital banks and fintech startups?

Recently updated on September 22, 2025

Core banking systems enable fintech companies to offer real-time transactions, personalized financial products, and seamless digital experiences. Modern core banking platforms improve scalability, security, and compliance, reducing operational costs while enhancing customer engagement through automation and AI-driven analytics.

What are the key features of a modern core banking system?

Recently updated on September 22, 2025

A modern core banking system includes features such as API integrations, real-time transaction processing, automated compliance reporting, digital onboarding, multi-currency support, and AI-powered risk assessment. These features help fintechs and digital banks provide efficient, secure, and user-friendly financial services.