Recently updated on April 21, 2026

In today’s fast-paced digital economy, the world of commerce is continually evolving, with businesses and consumers increasingly relying on electronic payments for their transactions. The payments market size is estimated at USD 3.16 trillion in 2025 and is expected to reach USD 5.30 trillion by 2030, at a CAGR of 10.88% during the forecast period (2025-2030).

At the heart of this financial ecosystem lies the entity known as the payment processor. While often operating behind the scenes, they play a pivotal role in enabling seamless and secure financial transactions, whether you’re making an online purchase, swiping your credit card at a local store, or conducting international trade.

This article aims to dig into the world of payment processors, unravel their intricate mechanisms, explore their critical role in any business, and give a step-by-step guide on how to become a payment processor.

What is a Payment Processing Company?

It is a financial institution or a third-party entity that manages the credit card transaction process, acting as a kind of mediator between the bank and its client. In other words, it transfers the information from the customer’s card to the bank and the customer’s bank. Assuming there are enough funds, the transaction goes through.

These types of companies play a crucial part in the financial industry’s payment sector as they provide secure and effective infrastructure and services needed to process various payments.

If you are running a small business, developing your own digital solution may not be financially possible. But without it, you`ll be able to accept payments only in cash or check, which are not favourable terms in a fast-growing digital world. That’s where a payment processor is extremely valuable. Such providers can take care of transferring money from digital channels, which include credit and debit cards and even digital wallets.

Why Would You Want to Become a Payment Processor?

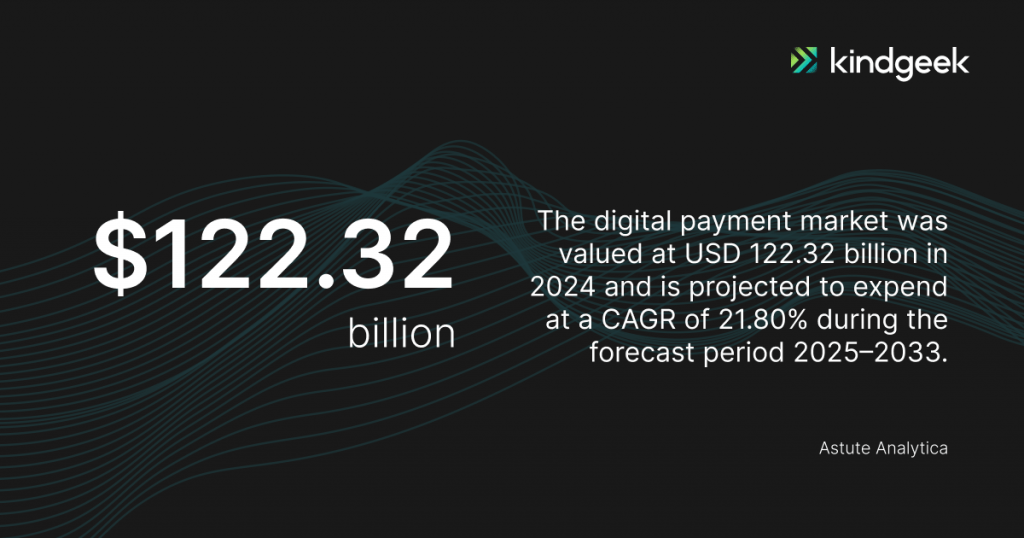

According to Astute Analytica, the digital payment market was valued at USD 122.32 billion in 2024 and is projected to hit the market valuation of US$ 712.14 billion by 2033 at a CAGR of 21.80% during the forecast period 2025–2033.

Even during the pandemic, when a lot of businesses were struggling to provide their services efficiently, this section of market was positively impacted by these circumstances. Customers across the world have shifted from offline shopping to real-time online ones during the pandemic, which has become one of the major factors driving the growth.

Amazon, eBay, and other e-commerce giants grew faster than expected. But so did the surrounding ecosystem, including payment platforms and buy now pay later operators. Within this ecosystem are dozens of payment processing companies, making it a profitable and fast-growing market with a large potential.

How Does a Payment Processor Work?

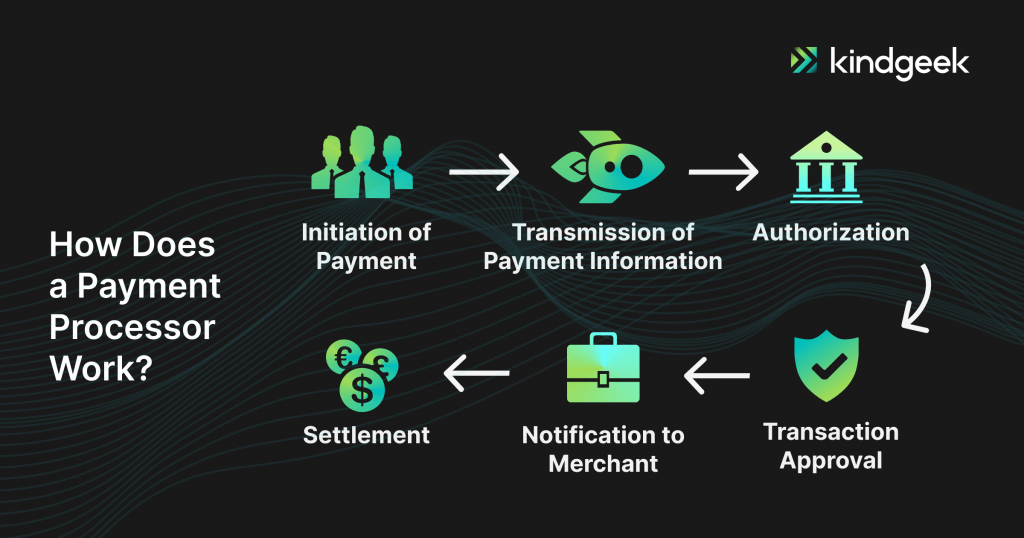

From the customer’s point of view, payment processing is a very quick and simple automated process. But if you dig deeper, it is, in fact, a multi-step process that manages billions of transactions daily, converting purchase intentions into completed sales within seconds. It includes customer authentication, authorizing, and settling the payment.

To make it more clear, let’s divide this process into steps:

Initiation of Payment

The process begins when a customer makes a purchase from a merchant, either online or in a physical store. The customer provides their main information, which typically includes credit card details, bank account information, or other methods like digital wallets (e.g., PayPal, Apple Pay).

Transmission of Payment Information

The information is securely transmitted from the merchant to the payment processor through the gateway, which encrypts and transmits the data.

Authorization

The payment processor’s first task is to check the validity of the customer’s data and assess whether the customer has sufficient funds or credit to complete the transaction. This is done by contacting the customer’s bank or card issuer. The payment processor sends an authorization request to the bank or card network, which either approves or declines the transaction.

Transaction Approval

If the customer has sufficient funds or credit, and there are no other issues (such as a stolen card or suspicious activity), the bank or card network sends an approval message.

Notification to Merchant

The payment processor informs the merchant whether the transaction was approved or declined. If approved, the merchant can proceed with delivering the product or service to the customer.

Settlement

After a successful transaction, the payment processor begins the settlement process. This involves transferring the funds from the customer’s account to the merchant’s account. It may not happen instantly and can depend on factors like the payment processor’s policies, the merchant’s agreement, and the type of method used.

Overall, a payment processor streamlines the journey, enhances security, and simplifies financial transactions for both merchants and customers, making it a critical component of the modern digital economy. Different payment processors may offer various features, support multiple methods, and operate in different regions, catering to the diverse needs of businesses and consumers.

Types of Payment Processors

Not all payment processors work the same way when handling digital transactions. Different types serve different functions within the broader ecosystem of digital payments. Let`s take a closer look at four key types to get a better understanding:

Front-end Payment Processors

Those are the most visible for merchants and customers. Front-end processors are responsible for managing the initial stages of a transaction – specifically, the authorization process. When a customer submits their card information at checkout, either online or in-store, front-end processors transmit the data securely and connect to the card networks to request authorization from the issuing bank. This process is designed to be fast, with approvals or rejections often delivered in just seconds.

In addition to basic transaction handling, modern front-end processors like Stripe, Square, and PayPal often provide a suite of tools for developers and merchants, including APIs, dashboards, fraud detection, and subscription billing support.

Back-End Payment Processors

This type operates behind the scenes. They don’t interact directly with customers but are crucial to completing a transaction. Once a payment is authorized, the back-end processor steps in to ensure that the funds are actually moved from the customer’s bank to the merchant’s account. This process, known as clearing and settlement, involves coordination between the issuing and acquiring banks and adherence to the rules set by card networks like Visa and Mastercard.

Major players in this space, such as FIS and Fiserv, often work with acquiring banks or large financial institutions to handle high volumes of transactions while maintaining compliance, handling chargebacks, and ensuring proper reconciliation.

Merchant Account Providers

A merchant account is a special type of bank account that businesses use to receive funds from card payments. Traditionally, setting up a merchant account was a separate step that required underwriting and approval. Merchant account providers assess risk, manage reserves, and give merchants a place to receive payments once they’re settled.

Providers like Worldpay and Helcim offer these services, often bundled with access to gateways and processing tools. However, newer platforms like Stripe have simplified this by grouping many merchants under a single large account, speeding up the onboarding process for small and medium-sized businesses.

Mobile Payment Processors

As its name suggests, this type is focused on enabling transactions through mobile devices. Whether through in-app purchases, contactless payments using NFC, or QR code scanning, mobile processors help create a seamless and fast experience for customers on the go. They support digital wallets like Apple Pay, Google Pay, and Samsung Pay and often offer APIs for app developers to integrate payment capabilities directly into their mobile platforms.

Mobile processors are especially valuable for retailers with physical stores, as well as companies that want to streamline in-app checkouts. They prioritize convenience and security, leveraging device-level authentication and encryption to protect user data.

How to Get Started with a Payment Processor: Steps to Become One

If you are asking a question: how to become a payment service provider and are planning to enter the payment processing market, there are two main ways to do so: build your software from scratch or choose a white-label solution for your company.

Building a software from scratch can be a difficult and time-consuming task, as it requires a lot of your resources and may take a few years to complete. You will also need a server infrastructure, robust security measures, and an expert development team capable of handling a complex fintech project.

Let’s figure out your steps:

Market Research and Planning

Before any “how to start a payment processing company”, it is essential to conduct thorough market research. In this case, it will help you to understand the payment processing industry, including its current trends, competitors, and potential opportunities. It will also be useful while defining your target market and the types of services you want to offer.

Creating a Business Plan and Registration

Based on the results of your market research, develop a comprehensive business plan that outlines your business model, revenue strategy, marketing plan, and financial projections. During this step, you should also determine the legal structure of your business and register it with the appropriate authorities.

Compliance and Regulations

During this stage, you should gain an understanding of the legal and regulatory requirements for payment processing in your jurisdiction and any regions you plan to operate in. Here, you should also gain the necessary licenses and permits.

Building Financial Partnerships

Establish relationships with banks or financial institutions that will facilitate the settlement of funds from transactions. Digital payment processing businesses often need a sponsor bank to work with.

Building Technology Infrastructure and Processing Platforms

Build or acquire the necessary technology infrastructure for payment processing, including secure servers, gateways, and fraud detection systems. During this stage, you will also build or acquire a transaction processing platform that can handle authorisation, settlement, and reconciliation of payments. Ensure that your platform supports various methods and currencies that you established in your business plan.

Testing and Launching

Conduct thorough testing of your payment processing system to ensure it works smoothly with different methods and devices. After all the testing, you are finally starting your payment processing company and processing merchant transactions. Continuously monitor and optimise your operations for efficiency and security.

Scaling and Expanding

As your business grows, consider expanding your services, entering new markets, and diversifying your offerings.

If you are going to choose your own payment processing or money transfer software development, consider Kindgeek. We provide core fintech banking and payment solutions to serve as a software shortcut for businesses looking to launch their fintech products, from digital wallets to neobanks, accommodating startups and enterprise-level customers.

The second option is choosing a white-label solution, which may significantly speed up your way to the market. That’s because you’ll have advanced software from the start without having to spend money, time and resources on developing one. The white-label solution gives you the opportunity to brand and customise the ready software according to your product needs.

It’s important to understand that you’ll still need to do proper market research to find a trustworthy solution provider that aligns with your expectations. In addition, working with a reliable vendor can help save your team resources and costs, plus reduce CAPEX (capital expenditures).

You will also need to take care of your business plan, registration processes, and bank account opening. All of the development stages will be skipped. That means that all you have to do once you’ve settled on the white label solution vendor is integrate it and onboarding your merchants.

The Cost to Start a Payment Processing Business

If you are researching how to be a payment processor, you are probably interested in finding out the costs. The establishment of a payment processing enterprise may require significant investment, with costs varying dramatically based on several critical factors. Rather than focusing on specific numbers, which can vary based on implementation approaches, understanding the underlying variables that influence these costs can provide a better understanding. Here are some of them:

Geographic Scope

If you plan to operate in a single country, it will be considerably less expensive than operating internationally. However, each additional market requires separate licensing, compliance frameworks, and banking partnerships.

Target Market Segment

For example, serving small merchants demands fewer resources than supporting enterprise clients. Another thing is that high-risk industries require more robust risk management systems and larger financial reserves, while specialized industries need custom solutions.

Business Model

The chosen approach significantly impacts costs. Full-service processors require comprehensive investments in technology and compliance. In other hand, partnership models or white-label solutions reduce initial expenses but may limit control and customization options.

Regulatory Environment

Highly-regulated markets demand extensive compliance infrastructure. While some regions have fewer initial requirements, changing regulations may introduce ongoing adaptation expenses.

Technology Approach

Proprietary systems offer complete customization but require extensive development resources, while licensed or cloud-based solutions provide faster implementation but include ongoing fees and potential limitations.

Conclusion

Payment processors play a pivotal role in modern commerce, seamlessly facilitating transactions and ensuring the smooth flow of funds in the digital age. Understanding the inner workings of payment processors is essential not only for businesses seeking to optimize their infrastructure but also for consumers who rely on secure and convenient methods in their daily lives.

The payment processing industry is not only desirable due to its potential for financial success but also because it underpins the global economy’s digital transformation. From compliance and technology infrastructure to partnerships and customization, becoming an online payment processing business requires careful planning, dedication to security, and adherence to industry regulations.

As the landscape of electronic payments continues to evolve, staying informed and adapting to new trends and technologies is a key on how to create a payment processing company. The world of payment processing is dynamic, and those who navigate it with expertise and innovation are able to play a pivotal role in shaping the future of commerce.

The future of payment processing will likely be shaped by several emerging forces: the continued globalization of commerce requiring cross-border solutions; the integration of alternative methods beyond traditional cards; embedded financial services that blur the lines between commerce and banking; and advanced fraud prevention leveraging artificial intelligence and machine learning. Processors that successfully navigate these trends will not merely facilitate transactions but help define the next evolution of money itself.

What does a payment processor do?

Recently updated on April 18, 2024

The payment processor transfers the information from the customer’s card to the bank and the customer’s bank, acting as a kind of mediator between the bank and its client.

What is the difference between a payment gateway and a payment processor?

Recently updated on April 18, 2024

A payment gateway is the initial point of contact for capturing payment information and ensuring its secure transmission, while a payment processor handles the behind-the-scenes processing, authorization, settlement, and management of the transaction.

How to become a payment processor?

Becoming a payment processor involves several steps and often requires compliance with various regulations and industry standards. Here are the general steps to becoming a payment processor: market research and planning, creating a business plan and registration, compliance and regulations research, building financial partnerships, building technology infrastructure and processing platforms, testing and launching, scaling and expanding.