Recently updated on April 18, 2025

If you are running a finance-related business, you must ask yourself one question – Do I know my customer? In an era marked by rapid digitization and globalized financial transactions, the importance of knowing your customer (KYC) to achieve compliance cannot be overstated. It’s not just a regulatory requirement, it’s a fundamental cornerstone of trust and integrity in the financial ecosystem.

In this article, we delve into the world of KYC, exploring its significance, key components, and the far-reaching consequences of both compliance and non-compliance.

What is KYC, and Why is it important?

KYC stands for “Know Your Customer” or sometimes can also mean “Know Your Client.” It is a process that financial institutions and businesses use to verify the identity of their customers or clients before cooperation and again periodically over time. Effective KYC involves knowing a customer’s identity, their financial activities, and the risk they pose.

KYC is required for any financial institution that deals with customers while opening and maintaining financial accounts. These institutions include banks, credit unions, wealth management companies, fintech apps, private lenders and lenders platforms, and others.

Banks are required to comply with KYC to limit fraud, but they also pass down those requirements to other businesses with whom they cooperate.

Fintech companies use KYC to ensure that:

- their clients are who they say they are.

- their clients fulfill the requirements to use certain financial services.

- their clients won’t use the product or platform for any illegal purposes.

- their clients will maintain a trustworthy, low-risk business relationship with them.

The main purpose of KYC is to prevent identity theft, money laundering, financial fraud, and other illegal activities.

Identity theft

KYC requires individuals to provide valid government-issued identification documents, such as passports or driver’s licenses, during the onboarding process. This helps ensure that the person opening an account or engaging in a transaction is the legitimate owner of the identity being presented. Some KYC systems even use biometric authentication methods to confirm a person’s identity, which is difficult for identity thieves to replicate.

Money laundering

KYC is a fundamental component of Anti-Money Laundering (AML) regulations and laws in many countries. It is a preventive measure against money laundering by establishing customer identities, scrutinizing their financial activities, and reporting suspicious behavior to authorities.

Financial fraud

KYC systems often use advanced technology to verify the authenticity of documents, including optical character recognition (OCR) and document verification software. This helps detect forged or altered documents, making it difficult for fraudsters to use fake IDs. KYC systems also often incorporate fraud detection algorithms that analyze customer behavior and transaction patterns to identify anomalies that may indicate fraud.

Ignoring the importance of KYC processes can lead to legal, financial, and reputational risks. In the first half of 2021 alone, 80 banks have been fined an estimated $2,732,099,008 for AML and KYC-related violations.

What’s the difference between KYC and AML

Anti-money laundering, or AML, is a framework of legislation and regulation financial institutions must follow. The primary purpose of AML is to stop obtaining financial income through illegal means.

The KYC process is a key part of the overall AML framework and specifically requires organizations to know who their customers or clients are and verify customer identity.

Overall, KYC is a subset of AML, with a specific focus on customer identification and verification. While KYC is concerned with establishing and maintaining accurate customer profiles, AML encompasses a broader set of activities aimed at detecting and preventing financial crimes, including money laundering and terrorist financing. Both KYC and AML are essential for financial institutions and businesses to protect themselves from the risks associated with illicit financial activities.

How to run an effective KYC program?

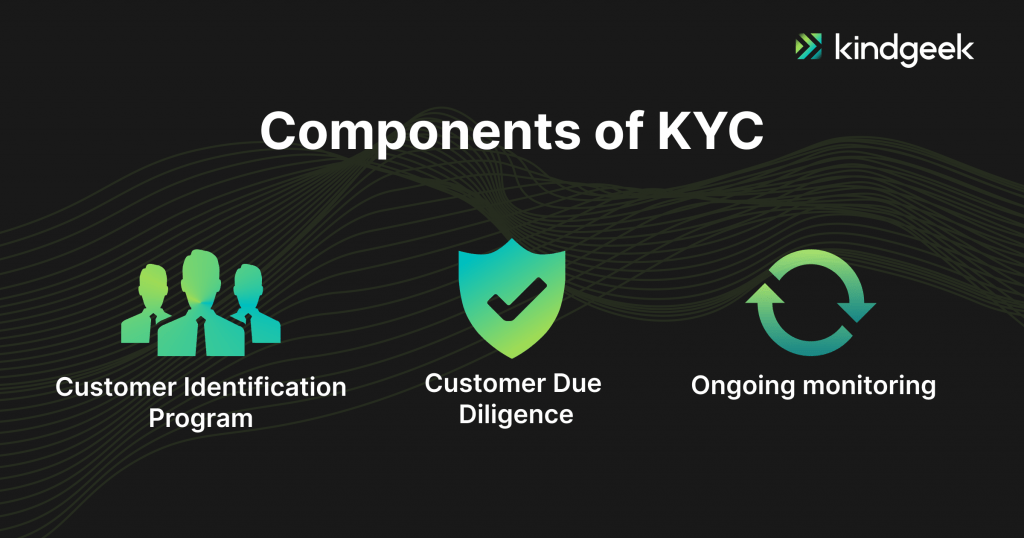

While the exact implementation process usually relies on the financial institution, a three-step approach for KYC is standard and specified in many countries’ regulations. It includes CIP (Customer Identification Program), CDD (Customer Due Diligence), and Ongoing monitoring.

These elements collectively form a comprehensive framework for KYC, which is crucial for preventing identity theft, financial fraud, money laundering, and other illicit financial activities while ensuring compliance with regulatory requirements.

Customer Identification Program

This involves verifying the identity of the customer or client. It includes collecting information such as name, date of birth, address, government-issued identification numbers (e.g., passport or driver’s license), and other relevant personal details.

In cases where the customer is an entity, KYC may require the identification of the beneficial owners or individuals who ultimately own or control the entity. This helps prevent the use of shell companies for illicit purposes.

A critical element to a successful CIP is a risk assessment that should be implemented both at the institutional level and at the level of procedures for each account. While the CIP provides guidance, it’s up to each individual institution to determine the exact level of risk and policy for that risk level. This helps financial institutions and businesses allocate resources appropriately for due diligence and monitoring efforts.

Proper collection, use, and storage of this data is also part of CIP requirements. Financial institutions should be able to verify collected information in a timely manner. Such procedures should be well documented and followed by all staff involved.

Customer Due Diligence

CDD is the process of assessing the risk associated with a customer and their transactions. It involves categorizing customers into different risk levels (low, medium, high) based on factors such as their source of funds, occupation, and transaction history.

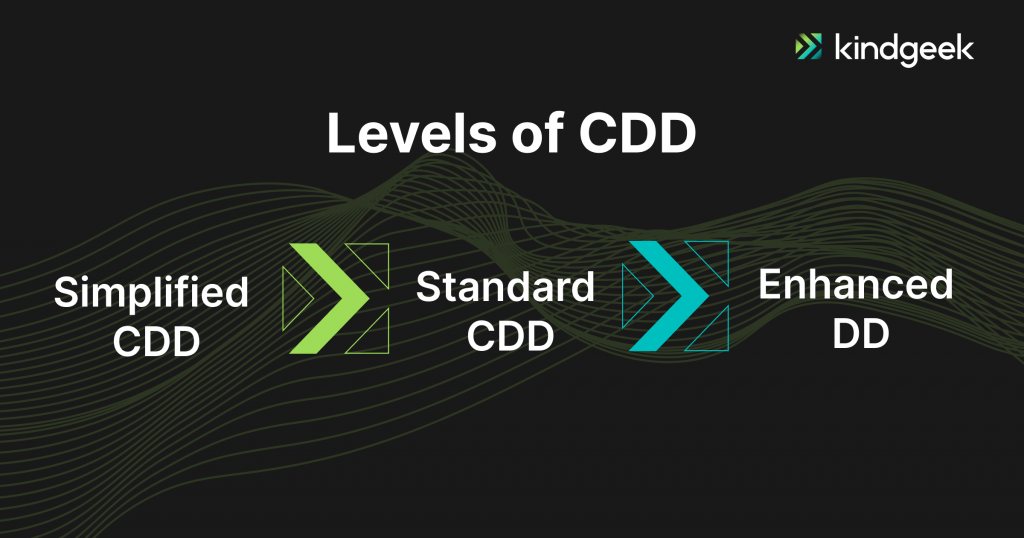

The levels of CDD can vary depending on regulatory requirements and the policies of the financial institution or business. However, there are three typical levels of CDD.

Simplified CDD

Simplified CDD is typically applied to customers who are considered low-risk. It involves a reduced level of documentation and verification compared to standard CDD. This may be applied to existing customers with a well-established relationship, small transactions, or certain types of entities that pose a lower risk of money laundering or financial crime.

Standard CDD

This is the basic level of CDD applied to most customers. It involves collecting and verifying essential customer information, such as name, address, date of birth, and government-issued identification documents (e.g., passport, driver’s license). Standard CDD is used for customers considered to be of low or medium risk.

Enhanced Due Diligence (EDD)

EDD is applied to customers or transactions that are considered to be of higher risk. This level of due diligence involves a more thorough examination of the customer’s background, source of funds, and transaction patterns. It may include additional document verification, ongoing monitoring, and a deeper investigation into the customer’s risk profile. EDD is typically used for politically exposed persons (PEPs), high-net-worth individuals, and entities in high-risk industries.

Ongoing monitoring

KYC is not a one-time process. It includes continuous monitoring of customer accounts and transactions to detect any suspicious or unusual activities. This helps identify potential fraud or money laundering attempts.

It also involves the real-time or periodic review of customer transactions for signs of suspicious activity, such as large cash deposits or frequent transfers to high-risk jurisdictions.

KYC compliance in the digital era

It’s no secret that the number of businesses entering digital marketplaces has grown dramatically over the past decade. That is why the interest in online KYC is growing as well. Although not every part of the KYC process could be outsourced, online customer verification solutions share a significant amount of compliance burden.

Digital KYS, also known as eKYC, is a modernized approach to customer due diligence (CDD) to verify their identity. That can be conducted online or digitally without face-to-face meetings or paper documents. By using different technologies such as document scanning (OCR), video calling, selfies (facial recognition), and biometrics, digital KYC provides a fast, efficient, and secure way that will benefit both customers and businesses.

According to Juniper Research, the spending on digital identity verification checks will reach $20.8 billion globally in 2027, up from $11.6 billion in 2022. It is an 80% growth over the five years.

What are the benefits of digital KYC?

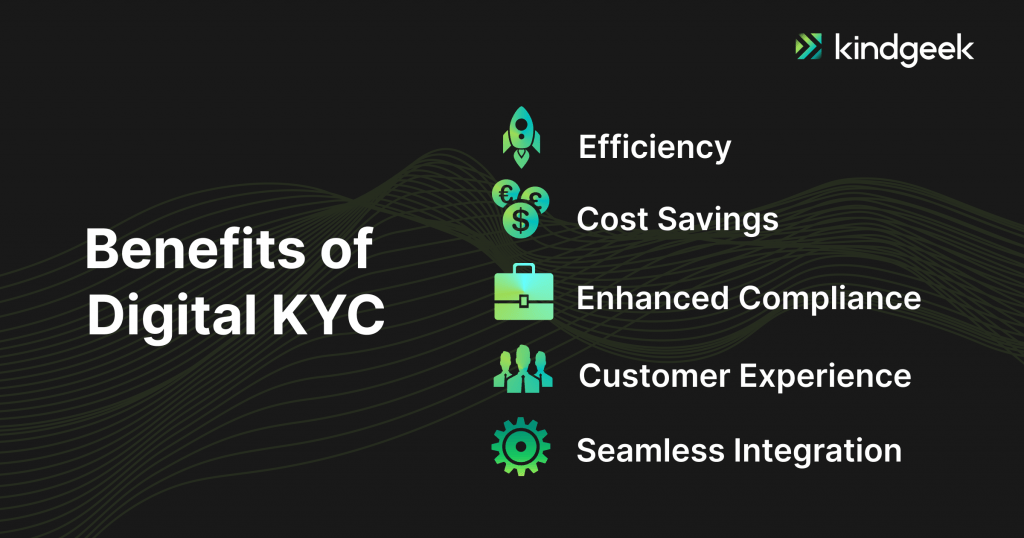

Digital KYC offers numerous advantages in terms of efficiency, accuracy, compliance, and customer experience. As technology continues to advance, digital KYC solutions are likely to become even more sophisticated and essential for businesses and financial institutions.

Efficiency

Digital KYC processes are often automated, allowing for quick and efficient customer onboarding. Customers can submit their information and documents online, reducing the need for manual data entry and paperwork. This convenience can lead to higher customer satisfaction and engagement.

Cost Savings

Automation of KYC processes can lead to cost savings for financial institutions and businesses. It reduces the need for manual labor, paperwork, and physical infrastructure, making operations more cost-effective.

Enhanced Compliance

Digital KYC solutions can be designed to incorporate compliance with relevant regulatory requirements automatically. This reduces the risk of non-compliance and associated penalties.

Customer Experience

Customers can complete the KYC process from any comfortable location, eliminating the need for physical visits to a bank or business location. This can improve the overall customer experience and reduce abandonment rates during account setup.

Integration with Other Systems

Digital KYC systems can integrate seamlessly with other banking or business systems, such as customer relationship management (CRM) and risk management systems, allowing for more comprehensive customer data analysis and risk assessment.

Conclusions

By implementing KYC procedures, businesses, and financial institutions aim to reduce the risk of being involved in illegal activities and protect themselves from potential legal and financial repercussions. KYC also helps build trust between customers and businesses by ensuring that legitimate customers are protected and that their personal and financial information is handled responsibly and securely.

If you are looking to build your own fintech solution with an effective KYC system built in, consider us. Kindgeek provides core fintech banking and payment services, general ledger software development, a number of white-label solutions and any custom software development that comes to mind. So don`t hesitate and contact us.

What is KYC?

Know Your Customer (KYC) is a process that financial institutions and businesses use to verify the identity of their customers or clients before cooperation and again periodically over time.

What are the components of KYC?

While the exact implementation process usually relies on the financial institution, a three-step approach for KYC is standard and specified in many countries’ regulations. It includes CIP (Customer Identification Program), CDD (Customer Due Diligence), and Ongoing monitoring.

What does AML stand for KYC?

KYC is a subset of AML, with a specific focus on customer identification and verification. While KYC is concerned with establishing and maintaining accurate customer profiles, AML encompasses a broader set of activities aimed at detecting and preventing financial crimes.