Recently updated on April 18, 2025

Banking as a Service (BaaS) is transforming how financial services are delivered by allowing fintechs to integrate banking products directly into their platforms through partnerships with licensed banks. This innovative model presents both opportunities and challenges for fintechs and traditional banks alike.

Each year, more financial institutions understand the importance of BaaS and integrate it into their services. The 2023 Finastra SOTN Report also proved this tendency. According to the survey, compared to 2022, decision-makers are considerably more likely to have either deployed or improved BaaS technologies within their organizations during the past 12 months, jumping from 35% to 48% year-on-year.

In this guide, we’ll explore the ins and outs of BaaS—how it works, the key advantages and potential drawbacks for fintechs looking to rapidly roll out banking offerings, and the benefits and risks for banks adopting this model to reach new customers and revenue streams.

Whether you’re a fintech company or a bank, this comprehensive guide will provide valuable insights into navigating the rapidly evolving BaaS landscape and leveraging this disruptive force reshaping finance.

Decoding the Concept of Banking as a Service

Let`s start with a Banking as a Service definition. BaaS is a type of cloud-bases solution which allows non-bank businesses, like platforms and marketplaces, to offer core financial services to their customers by integrating with banks via APIs.

So, how does Banking as a Service work? At the heart of any BaaS platform lies the core banking system, the engine that powers essential banking functionalities like account management and transaction processing. However, it’s the APIs that truly unlock the potential of BaaS, acting as secure gateways for third-party applications to seamlessly integrate and consume these banking services.

Businesses can leverage the platform’s payment gateway to facilitate secure financial transactions, accepting various payment methods from their customers. The lending and credit services component enables them to venture into the realm of loan origination and underwriting, offering products like personal loans or mortgages.

Ensuring regulatory compliance and mitigating risks are crucial in the financial domain, which is where the risk and compliance management component comes into play. It enforces protocols like KYC and AML, safeguarding against potential threats. Robust security measures, including multi-factor authentication and encryption, also ensure the protection of sensitive financial data throughout the ecosystem.

At first glance, it may sound similar to other technologies, such as open banking, neobanking, white-label banking or money transfer solutions. And even though they share some similarities, they have different purposes. Let`s make a small comparison.

Open banking is a regulatory framework that compels banks to securely share customer data and payment initiation capabilities with authorized third-party providers (TPPs). While BaaS models allow non-bank businesses to integrate complete banking services into their own products, Open banking models allow the same non-bank businesses to use the bank’s data for their products.

Neobanks, or digital banks, are still banks, but they operate entirely online without physical branches. They provide a modern and user-friendly banking experience primarily through mobile apps and online platforms.

White-label banking has an interesting and comprehensive approach. In this model, a bank or financial institution provides a complete banking solution, including technology, processes, and regulatory compliance, to a non-bank entity under the latter’s brand. The non-bank entity essentially acts as a front-end for the bank’s services, offering a branded banking experience to its customers. While BaaS provides specific banking capabilities through APIs, White-label Banking offers a turnkey solution for non-banks to offer full-fledged banking services under their own brand.

Money transfer software solution is a digital platform that enables users to send and receive funds electronically between accounts, often across different banks or even countries. These systems typically provide secure authentication, transaction processing, and confirmation mechanisms while offering various features like scheduled transfers, payment tracking, and integration with banking systems.

BaaS in Action for Fintech Companies

Banking-as-a-Service allows fintechs to leverage the infrastructure and expertise of established financial institutions without having to build everything from scratch. However, like any technology solution, BaaS comes with its own set of advantages and potential drawbacks. Understanding these pros and cons is crucial for fintech companies to make informed decisions and determine if BaaS aligns with their specific business goals and requirements. Let`s outline them in our article as well:

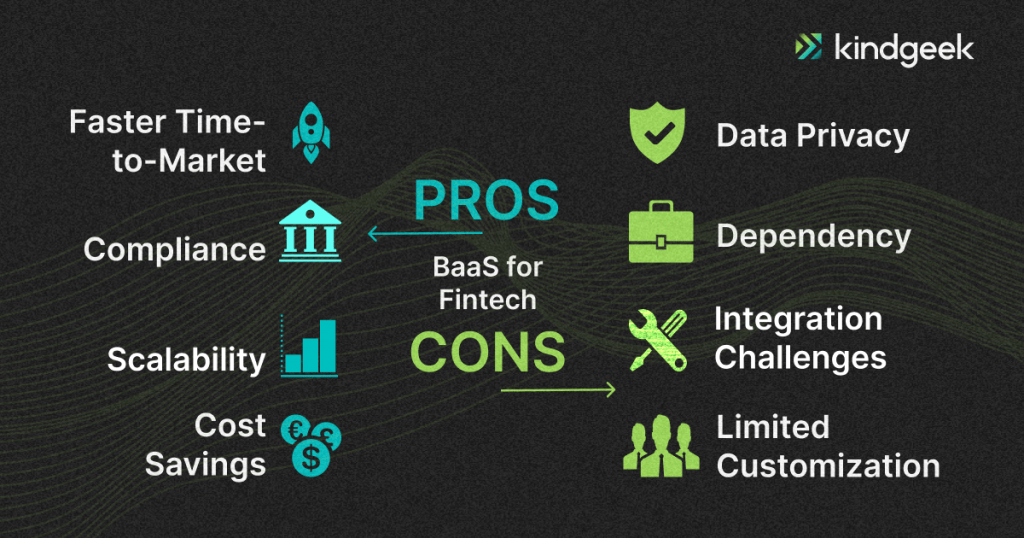

Pros:

Faster Time-to-Market

By leveraging BaaS, fintechs can quickly integrate banking services into their products without building the underlying infrastructure from scratch, allowing them to bring new offerings to market faster.

Cost Savings

BaaS eliminates the need for fintechs to invest in developing and maintaining complex banking systems, reducing operational costs and capital expenditures.

Compliance and Regulation

BaaS providers usually handle the complexities of regulatory compliance, such as KYC, AML, and data privacy regulations, alleviating the burden on fintechs and minimizing potential risks.

Scalability

Cloud-based BaaS solutions enable fintechs to scale their services up or down on demand, accommodating fluctuations in customer demand and business growth.

Cons:

Dependency on BaaS Provider

Fintechs become reliant on BaaS providers for the availability, reliability, and security of banking services, potentially introducing vendor lock-in risks.

Limited Customization

While BaaS offers some customization options, fintechs may have limited control over specific functionalities or the ability to tailor services to their unique requirements.

Integration Challenges

Integrating BaaS solutions with existing systems and processes can be complex, potentially requiring significant development efforts and resources.

Data Privacy

Despite the security measures implemented by BaaS providers, fintechs may have concerns about data privacy and the potential risks associated with sharing sensitive customer information.

Fintechs must carefully evaluate their specific needs, growth plans, and the trade-offs between the benefits of leveraging BaaS and the potential risks or limitations it may introduce. Different fintech companies such as Brex (a fintech focused on corporate credit cards and financial services for startups) or Robinhood (the popular investment app for commission-free stock trading) may serve as an example of striking the right balance between agility, cost-effectiveness, and control, which is crucial when considering BaaS as a solution.

BaaS in Action for Banks

Banking as a Service (BaaS) allows banks to leverage their existing infrastructure and capabilities to drive new revenue streams, foster innovation, and expand their reach. However, the adoption of BaaS comes with its own set of advantages and potential drawbacks that banks must carefully evaluate. Understanding these pros and cons is crucial for traditional financial institutions to make informed decisions and navigate the complexities of embracing the BaaS model. Let`s take a closer look:

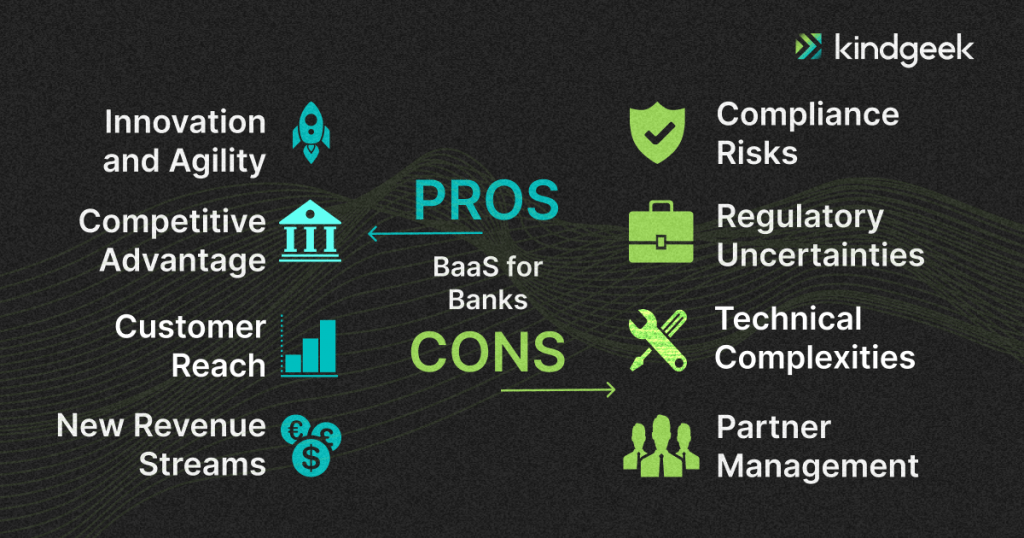

Pros:

New Revenue Streams

By offering BaaS, banks can monetize their existing infrastructure and technology by creating new revenue streams from non-banking entities seeking to embed financial services into their products or platforms.

Increased Customer Reach

BaaS enables banks to expand their customer base indirectly by powering fintech applications and services used by a broader audience, including tech-savvy consumers and businesses.

Innovation and Agility

Partnering with fintechs and other innovative companies through BaaS allows banks to leverage external expertise and agile development methodologies, fostering innovation and accelerating the delivery of new services.

Competitive Advantage

Offering BaaS can give banks a competitive edge, differentiating them from rivals and positioning them as technology leaders in the financial services industry.

Cons:

Security and Compliance Risks

Integrating with third-party systems and sharing data through APIs introduces potential security and compliance risks that banks must carefully manage and mitigate.

Technical Complexities

Implementing and maintaining a robust BaaS platform requires significant technical expertise, infrastructure investments, and ongoing maintenance efforts, which can be challenging for some banks.

Partner Management

Managing relationships with multiple BaaS partners, ensuring service level agreements (SLAs) are met, and coordinating integrations can be a complex endeavor for banks.

Regulatory Uncertainties

As BaaS is a relatively new model, there may be regulatory uncertainties or evolving compliance requirements that banks need to navigate, potentially increasing operational complexities and costs.

Banks must carefully evaluate their strategic objectives, technological capabilities, and risk appetite before embarking on a BaaS journey. While BaaS presents opportunities for revenue growth, innovation, and customer expansion, it also introduces challenges that banks must be prepared to address effectively. Different banks, such as Starling Bank and Cross River Bank, can serve as great examples of managing BaaS challenges while benefiting from its advantages.

Final Thoughts

In today’s rapidly evolving financial landscape, the Banking as a Service (BaaS) industry has emerged as a game-changing concept, reshaping the way traditional banking services are delivered and consumed. By leveraging the power of APIs and cloud-based technologies, BaaS enables banks to unbundle their offerings and provide modular banking capabilities to fintech companies and other non-bank entities.

By seamlessly integrating banking services into their platforms, fintechs can enhance their product offerings, streamline operations, and provide innovative financial experiences tailored to their customers’ needs.

On the other hand, by exposing their services through APIs, traditional banks can monetize their existing infrastructure, foster collaboration with fintech partners, and position themselves as technology leaders in the financial services industry.

As the financial services sector continues to evolve, the convergence of traditional banking and fintech innovation will shape the future of banking. BaaS stands as a powerful catalyst, enabling seamless collaboration, fostering digital transformation, and driving the development of innovative financial solutions that cater to the ever-changing needs of consumers and businesses alike.

If you are looking for a reliable partner to help you build a secure and successful financial product, consider Kindgeek. We are a full-cycle software development company with deep experience in fintech development. We can help you create a relevant and viable software product. Just contact us!

What is the BaaS definition?

BaaS meaning a type of cloud-bases solution which allows non-bank businesses, like platforms and marketplaces, to offer core financial services to their customers by integrating with banks via APIs.

What is BaaS in banking?

BaaS (Banking as a Service) in banking refers to the model where banks provide their core banking services and capabilities as API-driven offerings to third-party businesses and developers. Through BaaS, banks enable non-bank entities to integrate banking services into their own products or platforms without building the underlying infrastructure themselves.

What is the role of APIs in BaaS?

APIs act as secure gateways, allowing third-party applications and platforms to seamlessly access and integrate with the banking services offered by BaaS providers. APIs facilitate the exchange of data and functionality, enabling fintech companies to consume specific banking capabilities within their products or platforms.